It’s that time again when we need to select the best way of paying ourselves as directors and shareholders of our own company. This quick guide is to make sure you get things set up correctly and don’t end up losing out.

Please note this advice is for the 2021/22 tax year.

Although individual circumstances need to be taken into account, the vast majority of you will fall into the default setup. I’ll presume you have no other personal income that could affect these amounts. If this is not you, then you need to seek advice specific to your circumstances to ensure the most efficient setup.

You should also note that dividends can only be paid when a business has sufficient reserves. That is an accumulated profit over its history (even if that’s just the last month), less funds available to pay the tax currently due. Failure to do so may mean the dividends are not legal.

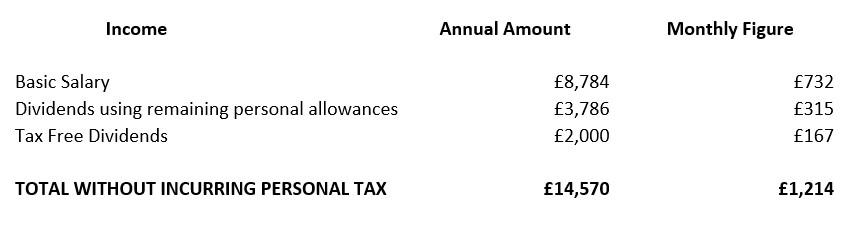

Setup to pay no personal tax

For some people paying a minimum salary and dividend combo that incurs no personal tax at all is the desired outcome. However, it is not necessarily the most tax-efficient method, especially if you still have spare profits.

The following table gives the setup for this:

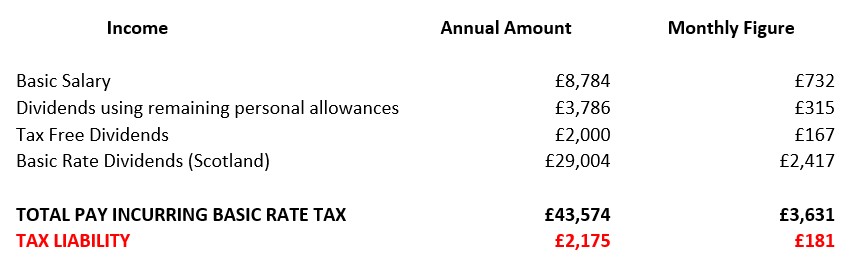

Setup to only pay basic rate tax

This is the most common setup for director/owners. It is a combination of salary and dividends that only exposes you to a maximum tax rate of 7.5%. You still have the option of additional dividends (profits permitting) but these will be exposed to the higher rate of tax of 32.5%.

Above this level

If you have profits beyond this level then paying dividends is not normally advised as a tax-saving measure. If the income is needed or desired and it is accepted that 32.5% of income will be lost as tax then it is not wrong to pay dividends, it’s just not necessarily a tax-efficient method.

If the income is not needed or desired then this may not be the best method of withdrawing funds from your company. You should consider other withdrawal routes and tax savings measures that may be open to you such as pension contributions and use of home as office agreements. As the tax at stake at these levels is quite high you should seek professional advice before committing to anything.

If you need further help or guidance around efficient tax planning then get in touch.

Let’s Chat

Susan Crichton

SJC+0 Accounts

07957 581757

susan.crichton@sjcplus0.co.uk